Section 8 Company Compliance

4.9

Section 8 Company Compliance - Process, Fees, Documents & Penalties

A Section 8 company in India is a non-profit organization that promotes social welfare under the Companies Act, 2013. Section 8 companies, like other businesses, must comply with certain criteria. Regardless of their non-profit status and commitment to helping others, these companies must follow particular regulatory requirements.

The purpose of forming Section 8 Company is to promote, encourage, and nourish activities related to art, science, sports, commerce, charitable activities, etc. Section 8 Company can be categorized as a Non-Governmental Organization. These companies enjoy the liberty of being treated as ‘Limited Company’, though, word ‘Limited’ is not added at the end of their names. Concisely, Section 8 companies work in the direction of promoting needy communities and sectors in India. These Companies are not liable to give income or dividend to its members.

Table of Content

- What is Section 8 Company?

- Benefits of Section 8 Company Compliance

- Documents Required for Section 8 Company Compliance

- List of mandatory Section 8 company compliances

- Event-based Annual Compliances of Section 8 Company

- Penalties to be charged in case of Non-Compliance

- Due Dates for filling Section 8 Company Compliances

- Conclusion

- Frequently Asked Questions

What is Section 8 Company?

In India, a Section 8 company is a non-profit organization that serves the goal of promoting commerce, science as well as social welfare research, and conservation of the environment. If you are granted authorization, you can operate your business and make profits. But, you are not able to share the profits among the members of your business.

All Section 8 company is required to perform the annual compliance procedures outlined under the Companies Act of 2013 and the Income Tax Act of 1961. This ensures the company's credibility and trustworthiness and avoids fines for non-compliance. For instance, compliance obligations to be performed during the year can be time-consuming. In the case of non-compliance, could result in severe sanctions, which could impede directors' positions within the firm.

Benefits of Section 8 Company Compliance

As a non-profit organization striving for social welfare or generating a beneficial influence, section 8 company registration comes with considerable benefits, as indicated below:

- Tax Exemptions: One of the most important benefits of Section 8 company compliance is tax exemption. Companies in this category are free from income tax charges on extra income that conforms to the organization's objectives.

- Company Compliance & Regulation: Company compliance ensures that your business complies with the legal framework. The mere existence of compliance functions as evidence that you uphold the commitment to practicing ethical principles and abide by the legal declaration.

- Access to Funding: Section 8 Company Compliance is how you get money from the government or non-governmental groups. Compliance provides you with endless opportunities to obtain investment, increase your presence, and pursue innovative solutions. It is essential for increasing your organization's influence and impact.

- Avoiding Penalties: Section 8 Company compliance helps you avoid penalties. However, noncompliance has a negative influence on the license, which can be canceled, confiscated, or cause the establishment to close.

Documents Required for Section 8 Company Compliance

The documents required for Section 8 company compliance are extremely important; without them, you cannot operate. Nonetheless, the following are the required documents indicated below:

- Articles of Association

- Memorandum of Association

- Digital Signature Certificate

- Company Incorporation Certificate

List of Mandatory Section 8 Company Compliances

Section 8 companies must follow legal and regulatory compliances:

- Appointment Of Auditor: It is compulsory for a Section 8 company to appoint an auditor to take care of their financial recordings every year.

- Maintaining Registers: Maintaining statutory records in registers is expected from Section 8 companies. These registers are maintained on a year basis and the purpose of these registers is to check how the company has performed annually. Information related to members, loans, charges and investment is provided in the register.

- Maintenance Of Financial Statements: Financial records of a Section 8 Company are maintained on an annual basis. Once the financial records are prepared they are presented in the front of the registrar. Financial records consist of the following information:

- Trading Account

- Profit and Loss Account

- Balancesheet

- Preparing Director’s Report: Section 134 of the Companies Act, 2013 says that Form AOC-4 is needed to file the Director’s Report. The purpose of preparing a Director’s Report is to give shareholders a preview of the financial position of the company and the scope of its business. The signed ‘minutes of meetings’ is required to be maintained at the Registered Office.

- Income Tax Return Filing: Section 8 company are required to file for Income Tax Returns on or before 30th September of the next fiscal year. In order to give complete overview of the company’s income it is essential to file for Income Tax return. But if the company is registered under Section 12A and 80G it can avail the benefit of tax exemption.

- Conduct Board Meeting: Board meeting of every company should be held twice a year in case of small companies. The gap between the two meetings should not be more than 90 days.

- Conduct Annual General Meeting: Annual General Meeting of the Section 8 Company should be held yearly on or before 30th September. It is necessary for all the directors, members, and auditors to attend the meeting. They should be notified regarding the meeting by giving not less than 21days notice. Form MGT-15 is used to submit the report of Annual General Meeting. The report must be submitted within 30 days of conducting the meeting.

- Filing Of Financial Return With RoC: E-form AOC-4 is used to file the copy of financial statements. It is filed within 30 days from the date on which the annual general meeting is held.

- Filing Of Annual Return With RoC: Form MGT-7 is used to file the annual return of the company. Annual return is filed within 60 days from the conclusion of the Annual General Meeting. Where at whatever year no Annual General Meeting is held, the yearly return ought to be recorded inside sixty days from the days on which the yearly General Meeting ought to have been held that is 30 September. It ought to be connected with the announcement referencing the explanations behind not holding the Annual General Meeting.

Event-based Annual Compliances of Section 8 Company

Event based, as the name recommends, are the compliances should be documented on the event of explicit occasions. In contrast to annual compliances, these are non-periodical in nature.

Checklist For Event-Based Compliances For Section 8 Company:

- Transfer of shares

- Appointment/Resignation of Directors

- Appointment/Resignation of Auditors

- Modification in company’s name

- Modification in company’s MOA

- Appointment of Key Managerial Personnel

- Receipt of share application money

- Any alteration in the company’s structure

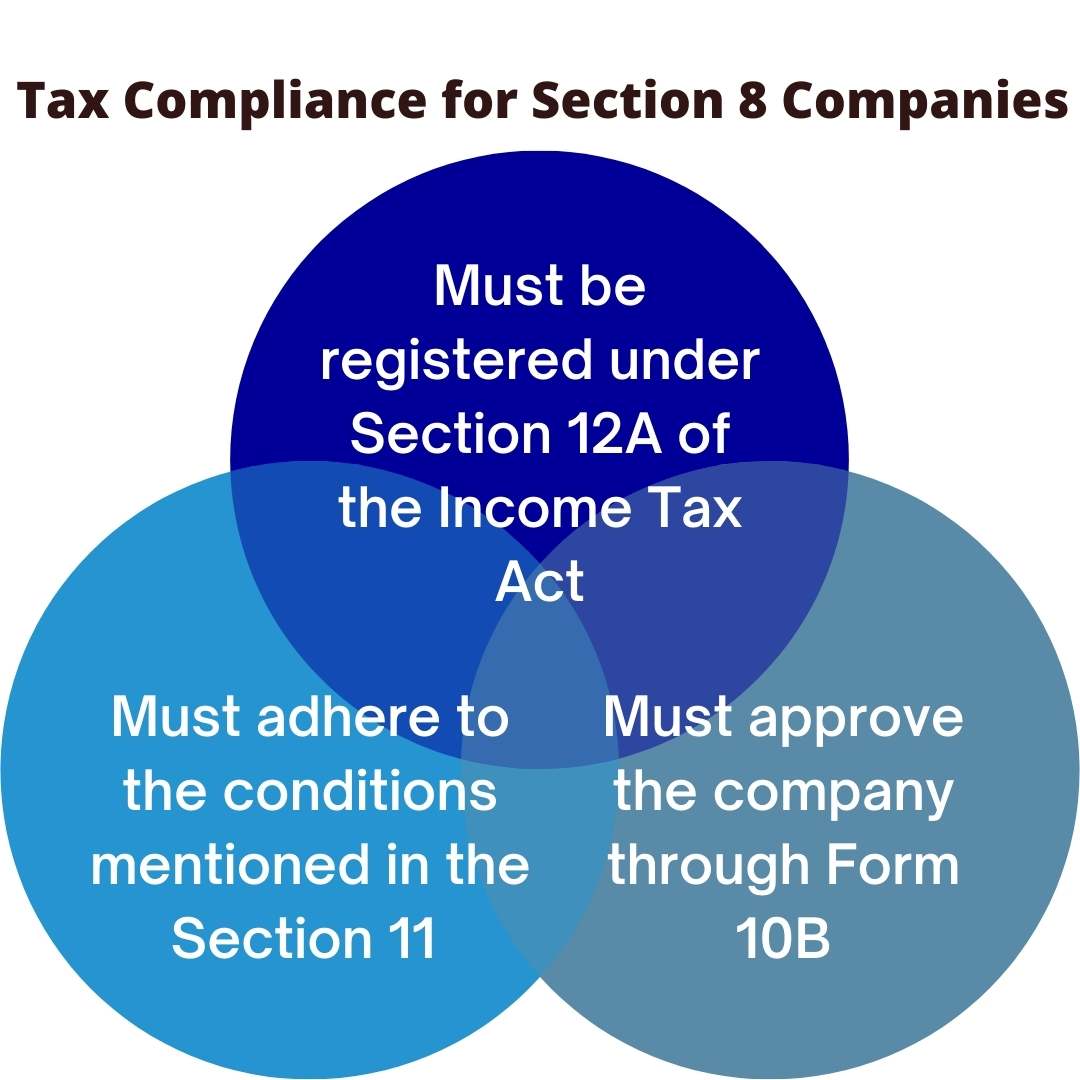

Tax Compliance for Section 8 Companies

Section Company is bound to pay corporate tax as mentioned in the Income Tax Act. But by adopting certain measures the Company can exempt its certain income from the income tax. To entertain such exemptions Section 8 Company needs to fulfil the following compliances:

- Section 8 companies must be registered under Section 12A of the Income Tax Act, with the Principal Commissioner using form 10A.

- It must adhere to the conditions mentioned in the Section 11 if the company wants to fall under the criteria of eligibility for the exemption.

- Section 80G must approve the company through Form 10B.

Penalties to be charged in case of Non-Compliance

The Ministry of Corporate Affairs has the authority to impose certain penalties in case it encounters any non-compliance with the procedures.

Penalties to be imposed are as follows:

- License Revocation: The Central Government may disavow the permit allowed to the organization on the off chance that it finds that the organization is working falsely or in a way violative to the object of the organization.

- Penalty on Company: The organizations will be culpable with fine, which will not be under ten lakh rupees and can be stretched out to one crore rupees.

- Liability of Directors: The chiefs and each official of the organization who is in default will be culpable with detainment for a term which may stretch out to twenty-five lakh rupees or with both.

- Fraudulent ConductIn the event that it is discovered that the issues of the organization were directed falsely, every official in default will be at risk for activity under area 447.

Due Dates for filling Section 8 Company Compliances

Non-compliance can lead to penalty and for the Section 8 Company the best way to ignore penalty is quite smooth, all the company has to do is follow the compliances within the stipulated period of time.

| COMPLIANCE | DUE DATE |

|---|---|

| AGM (Annual General Meeting) | 30thSeptember |

| AOC-4 | Within 30 days of AGM |

| MGT-7 | Within 60 days of AGM |

| Income Tax Return | 30th September |

Note: The aforementioned Fees is exclusive of GST.

Conclusion

Annual compliance requirements for Section 8 companies are not just a legal requirement, but also a way to capitalize on the benefits that come with its status. By strictly complying to these requirements, Section 8 firms can avoid the penalties associated with noncompliance, assuring their continuing operation and commitment to their specific social goals. Professional Utilities streamlines Section 8 corporation compliance. Our professionals ensure that your non-profit organization follows all the rules and regulations outlined in the Companies Act 2013. We handle everything, from submitting documents to maintaining records and compiling financial statements, so you may focus on your nonprofit activity. We may help you avoid penalties and remain compliant.

Frequently Asked Questions

Can Section 8 Company be incorporated both as Private and Public Limited Company?

Yes, it is the candidate's decision to incorporate a Section 8 Company as a private or public limited company in the wake of meeting the consistence necessity for example 2 Directors and 2 individuals if there should arise an occurrence of privately owned business and 3 Directors and 7 individuals in the event of Public Limited Company. However, One Person Company (OPC) can't be joined as a Section 8 Company according to Rule 3 of the Companies (Incorporation) Rules, 2014.

Are there any prescribed criteria with respect to Minimum and Maximum number of directors in a Section 8 Company?

The prescription under section 149(1) of Companies Act 2013 as to having Minimum of three directors for public limited company and two directors for private limited company and maximum of fifteen directors is not applicable to section 8 company and thus there is no prescription with respect to minimum or maximum directors in a section 8 Company. However, second proviso to section 149(1) requires a woman director in prescribed class of companies. Also section 149(3) requires every company to have a resident director.

Are Secretarial standards applicable on a Section 8 Company?

No, there is a particular exemption to Section 8 and One Person Company from conforming to the Secretarial Standards. In any case, Companies must hold fast to Secretarial norms so as to raise the corporate governance standards.

Tax Benefits: Section 8 Company is a non-benefit association that is the reason they are excluded from certain arrangements of the personal expense. They are additionally given various different conclusions and other tax reductions. One of such exclusion is under Section 80G of the Income Tax Act, 1961, whereby contributors to non-benefit associations may guarantee a half discount against gifts made. The registration done under Section 80G will be legitimate for regularly a time of one-three years.

What happens if I don’t file my Annual Return?

Inability to document Annual Returns is punishable with a fine of Rupees 50,000 which may stretch out to Rupees five lakh.

Is it possible for a foreign Company to be registered as a Section 8 Company in India?

Section 2(42) of the Companies Act, 2013 defines the term “Foreign Company” and means any company or body corporate incorporated outside India which– (a) has a place of business in India whether by itself or through an agent, physically or through electronic mode; and (b) conducts any business activity in India in any other manner. Now since a Company or a body corporate incorporated outside India for doing not for profit activit es, which has opened a branch/liason office in India, cannot fall in definition of a foreign company as business activity is missing. Therefore, such company cannot be termed as foreign company. However, subject to compliance of FEMA regulations, it can open branch/liason offices. Such not for profit companies or bodies corporate incorporated outside India can promote and register a Section 8 Company in India as a distinct entity.

Can a Society registered under the Societies Registration Act, 1860 be registered/converted into Section 8 Company?

Yes. Section 8(1) of the Companies Act, 2013 allows person or association of persons to be registered as a Section 8 Company on fulfilment of certain conditions and procedure as prescribed therein. The term “person” has not been defined in the Companies Act, 2013. Section 2(41) of the General Clauses Act, 1897 provides that “person” shall include any Company, or association or body of individuals, whether incorporated or not. Accordingly, a Society registered under the Societies Registration Act, 1860 is a person. Therefore, Society can be registered/converted as a Section 8 Company.

Is there any relaxation in Stamp duty payment on issuance of share certificate by a Section 8 Company?

Stamp duty on issue of share certificates is governed by Indian Stamp Act, 1899 as adapted by respective state or stamp act of respective state, as the case may be. No relaxation of special rate of stamp duty has been provided by any of the state in respect of stamp duty payable on issue of share certificates by Section 8 Company.

Can Section 8 Companies receive contributions from overseas or non-residents?

There are special requirements to be complied with under the Foreign Contribution and Regulation Act, 2010 before a Section 8 Company can receive any contributions or donations from overseas/outside India from non-residents. The provisions of the said Act are in addition to the provisions under the Companies Act.

Disclaimer:The information provided on this website is intended for general information purposes only. Although all reasonable efforts are made to ensure that the information provided is correct and reliable, it is not advised to be used as a substitute for professional advice. The information herein is not to be used in place of seeking professional services, counsel, or guidance. We highly advise that you consult a professional before you make any business or legal decisions regarding the information presented on this website. This website and its contents are given "as is", and we do not take any responsibility for any action that is taken based on information given on this website.

- Written by: Abhishek Yadav

- Fact-checked: Sahil Singh

- Updated on: April 04, 2026

Testimonials

"Explore how Professional Utilities have helped businesses reach new heights as their trusted partner."

It was a great experience working withProfessional Utilities. They have provided the smoothly. It shows the amount of confidence they are having in their field of work.

Atish Singh

![]()

![]()

It was professional and friendly experience quick response and remarkable assistance. I loved PU service for section 8 company registration for our Vidyadhare Foundation.

Ravi Kumar

![]()

![]()

I needed a material safety data sheet for my product and they got it delivered in just 3 days. I am very happy with their professional and timely service. Trust me you can count on them.

Ananya Sharma

![]()

![]()

Great & helpful support by everyone. I got response & support whenever I called to your system. Heartly thanx for Great & Super Service. Have a Great & Bright future of team & your company.

Prashant Agawekar

![]()

![]()

Thank you so muchProfessional Utilitiesteam for their wonderful help. I really appreciate your efforts in getting start business. Pvt Ltd company registration was smooth yet quick.

Abhishek Kumar

![]()

![]()

I applied for Drug licence and company registration and their follow-up for work and regular updates helped me a lot. They are happily available for any kind of business consultancy.

Vidushi Saini

![]()

![]()

Great experience went to get my ITR done, process was quite convenient and fast. Had a few queries, am happy about the fact those people explained me all things I wanted to know.

Taniya Garyali

![]()

![]()

Great services provided by Professional Utilities. They are best in this industry and the best part is their prices are so affordable. Kudos to you. Now you guys are my full-time consultant.

Aftab Alam

![]()

![]()

Trusted By

.svg)