Cancellation of GST Registration means that the taxpayer will no longer be able to pay or collect Goods and Services Tax.

The registration under GST can be cancelled for various reasons. The cancellation can be initiated either by the tax officials or the registered taxpayer can apply for the cancellation of the GST Registration.

In case of death of a registered person, the legal heirs can apply for the cancellation.

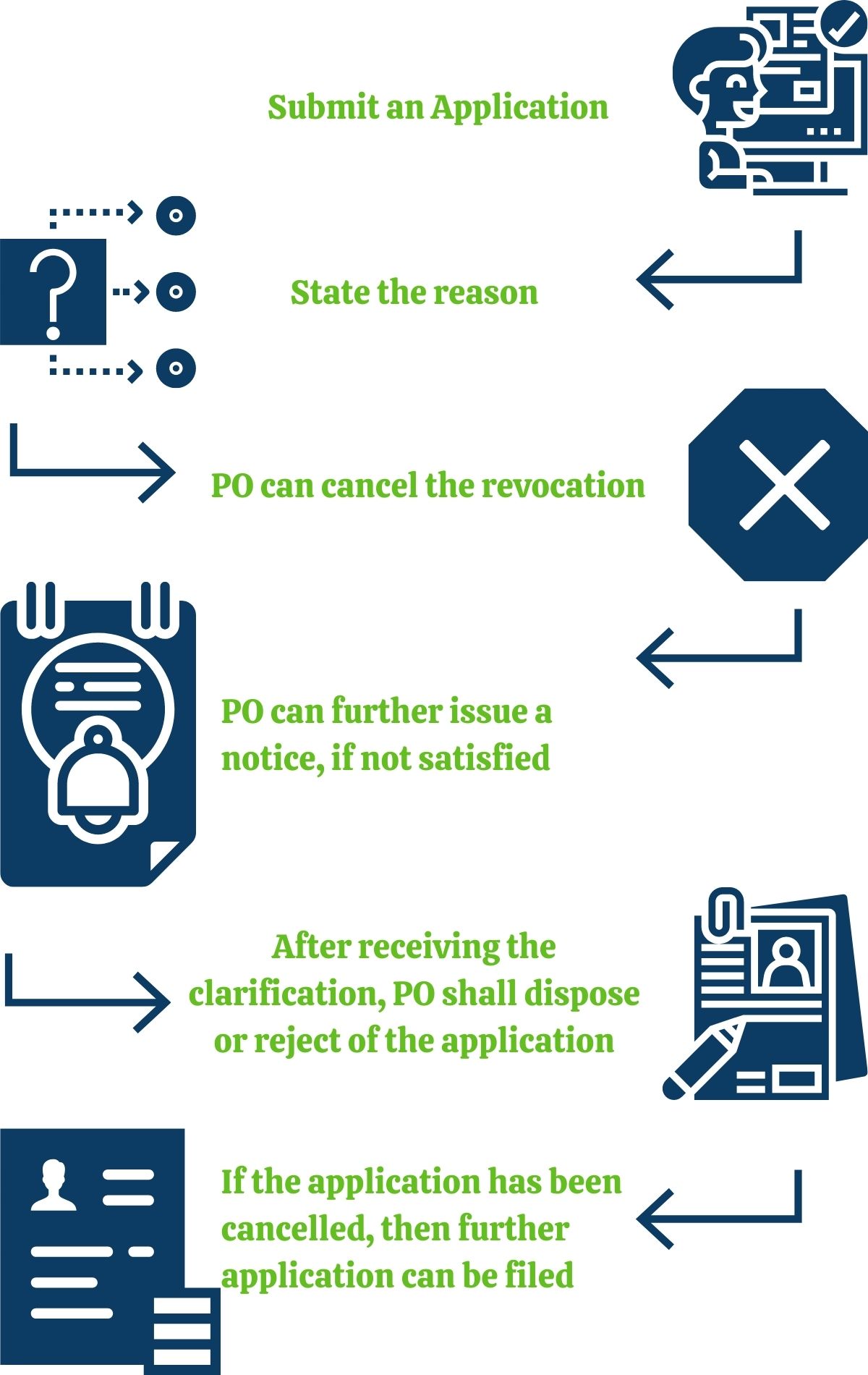

There is a provision for revocation of the cancellation if the registration is cancelled by the department. We'll cover it in this article.

The registration can be cancelled for three main reasons:

Revocation means official cancellation of a decision. If the GST Registration is cancelled by tax officials on their own motion, then the registered person can apply for the revocation of cancellation of registration within thirty days from the date of cancellation order.

Call us on

+91 9821113117

[Mon - Sat, 10am - 7pm]

Write to us

![]() 8th Floor, Bhandari House - 91, 804,

8th Floor, Bhandari House - 91, 804,

Nehru Place, New Delhi 110019

![]() Reliable

Reliable

![]() Affordable

Affordable

![]() Assurity

Assurity

They've been very helpful in our registration with ICEGATE. It was a small thing with a small amount paid which somehow escalated to a very painful procedure. Never did they say "You've only paid so much. It's too much effort for us.".

Very pleased with their service. Prompt, professional and great communication. Definitely recommend. Special mention for Ms. Razia - she handled our case.

Professional Utilities is fully professional in their work, Rates are too low and genuine. Services and satisfaction are high so I highly recommended Professional Utilities.

They are one of the most genuine and reasonable people. I applied for lmpc certificate through them and they charged me a very nominal amount as compared to what other firms asked .